What Enterprise IT Buyers Are Actually Doing About Tariffs

Key Takeaways

-

35% of technology leaders have moved beyond monitoring tariffs into active planning or adjustment.

-

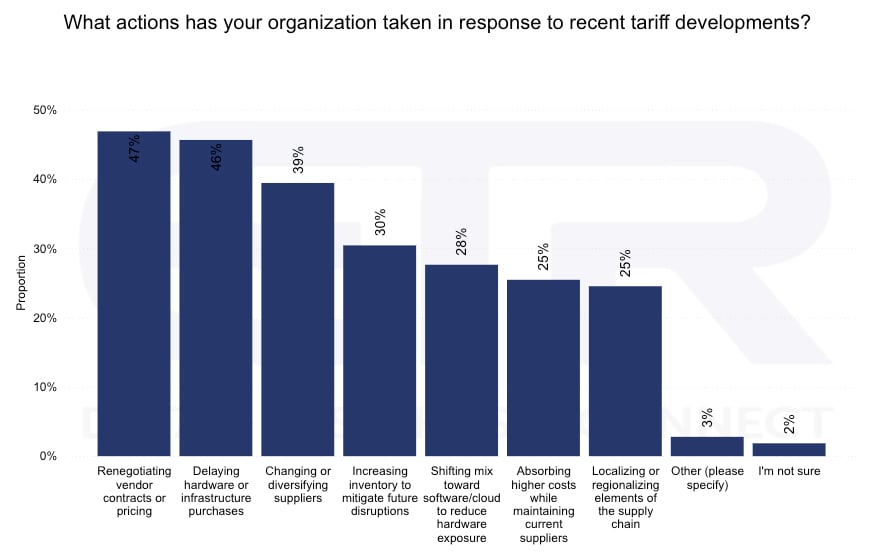

Contract renegotiation leads the response at 47% of acting organizations, followed by hardware delays at 46%.

-

Hardware spending is surging, but likely reflects tariff-driven pre-buying rather than durable demand.

-

Software pricing (3.3%) is moving opposite to hardware pricing (5.5%), making cloud and SaaS the structural hedge.

-

The 55% still watching represent a forward indicator, not a permanent baseline.

In ETR's Spring 2026 Macro Views Survey (a quarterly study of enterprise IT spending intentions among 1,709 technology leaders, including 288 Fortune 500 and 421 Global 2000 organizations), 35% of enterprise IT buyers have moved beyond monitoring tariffs into active adjustment. Contract renegotiation and hardware delays lead the response, with 47% and 46% of acting organizations taking each step. Three percent have already implemented material changes.

The broader budget picture reinforces the urgency. Calendar year 2026 (CY2026) IT spending growth fell to 3.6%, down from 4.6% in the Winter 2026 Macro Views Survey, with the slowdown running across enterprise sizes, industries, and regions. Tariffs are showing up in contracts, hardware timing, and supply chain strategy in ways the data makes difficult to dismiss.

How Are Enterprise IT Buyers Responding to Tariffs?

The tariff response data divides the market more cleanly than most headlines suggest.

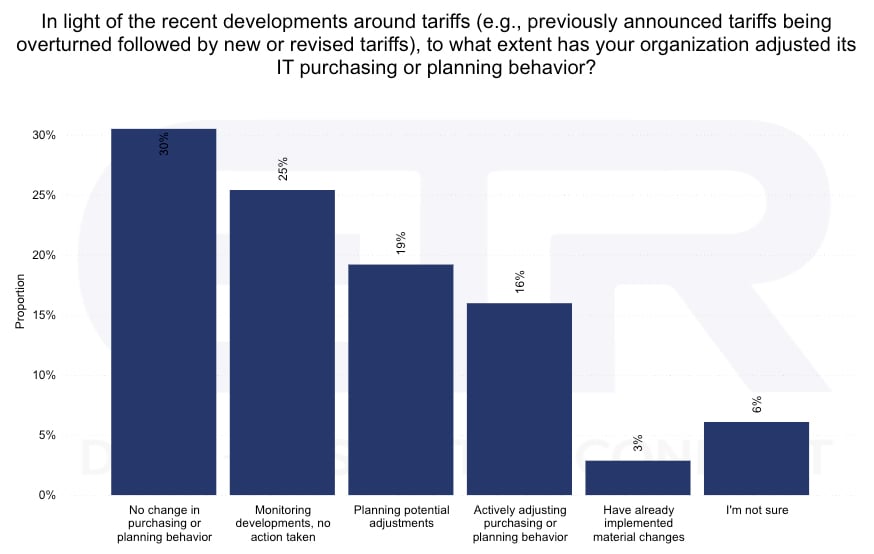

Thirty percent of technology leaders report no change in purchasing or planning behavior. Twenty-five percent are monitoring developments but have not yet acted. Together, 55% of the market is in a holding position, a meaningful counterweight to overheated narratives about tariff-driven disruption.

The remaining 45% have engaged in some form of response. Nineteen percent are planning adjustments; 16% are actively adjusting purchasing or planning behavior. Combined, 35% of technology leaders have moved beyond monitoring. Three percent have already implemented material changes, a small share, but one that identifies which accounts are leading the curve.

Among organizations taking action, renegotiating vendor contracts leads at 47%, followed closely by delaying hardware and infrastructure purchases at 46%. Changing or diversifying suppliers comes in at 39%. Shifting toward software and cloud to reduce hardware exposure is underway at 28%, with absorbing higher costs and localizing supply chain elements each at 25%.

Contract renegotiation and hardware delays work together. Buyers are using tariff exposure as the lever to reopen pricing on what they are already deploying and to pause what they have not yet committed to. Supplier diversification at 39% adds a third dimension: organizations are willing to absorb switching costs to reduce concentration risk, and single-region supply chains are being treated as liabilities in ways they were not twelve months ago.

Why Is Hardware Spending Surging While Buyers Are Delaying Purchases?

Hardware is the most complicated narrative in the spring report, and the one most directly shaped by tariff dynamics.

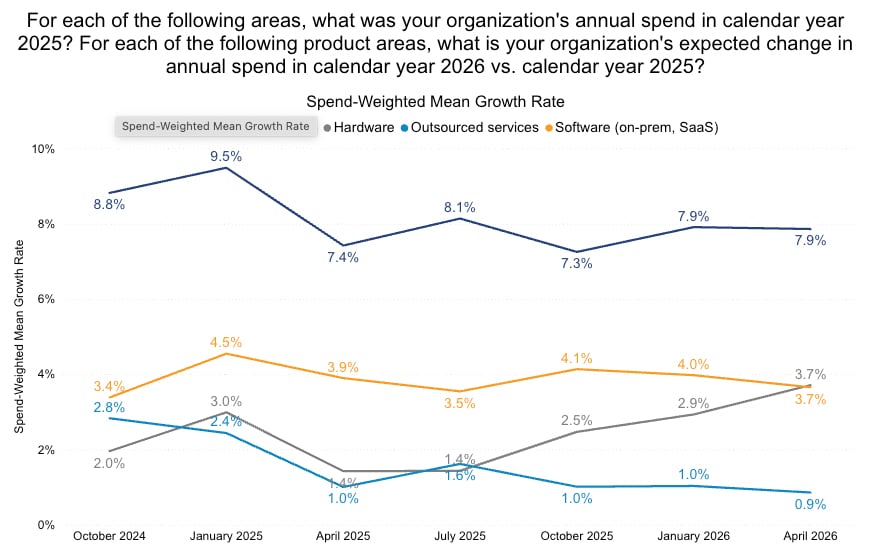

Hardware spending accelerated to 3.7%, its highest level since October 2024, while hardware pricing surged to 5.5%, up nearly two percentage points from winter and the sharpest pricing increase of any major category. Both numbers are rising at the same time. That is not a coincidence.

The most plausible interpretation, consistent with ETR's read of the data, is tariff-driven pre-buying: organizations pulling forward hardware purchases they had already planned ahead of anticipated price increases. "Increasing hardware spending" rose to 13% as a primary increased-spending lever, its highest point in the Macro Views Survey series.

"The signal in the data is not that buyers are panicking. It is that they are repricing the relationship."

For hardware-exposed vendors, the demand picture deserves scrutiny. Pre-buying pulls revenue forward; it does not create new revenue. Forecasts that treat Q1/Q2 hardware strength as durable demand are likely overestimating the back half.

Why Are Buyers Shifting Toward Software and Cloud to Avoid Tariff Exposure?

Twenty-eight percent of acting organizations are shifting toward software and cloud to reduce hardware exposure. It is the only structural response in the data, not a tactical adjustment to existing plans, but a deliberate change to how organizations are building their stacks.

The price dynamics support it. Cloud infrastructure and platform services (IaaS/PaaS) is holding at 7.9% growth. Security software leads all subcategories at 7.2%. Software pricing has eased to 3.3% while hardware pricing surges to 5.5%. The gap is widening, and procurement behavior is beginning to follow.

The tariff effect on software and cloud will not show up in this quarter's bookings. It will show up in 18-month infrastructure roadmaps. For vendors in tariff-insulated categories, the competitive narrative is available: the pricing story supports an explicit claim that SaaS and cloud are the lower-volatility line item in any stack review. For buyers evaluating substitution, this hedge works on a 12-to-24-month view, not a quarterly one.

The Budget Backdrop: Why Tariff Pressure Is Landing Harder in 2026

Enterprise IT spending entered the year with momentum. The Winter 2026 Macro Views Survey showed CY2026 spending growth expectations at 4.6%, and 74% of respondents planned to increase IT spending, the highest January reading since 2022.

Spring refined that picture. Spending growth fell across enterprise sizes, industries, titles, and regions. Fortune 500 expectations pulled back from 4.0% to 3.2%. Vendor consolidation is rising. SaaS license optimization hit a series high. The buyer question has changed: not only "Should we buy this?" but now "Should we keep this, expand this, consolidate this, or replace this?"

That environment makes tariff exposure land differently than it would in a growth market. When every line item is under scrutiny, tariff-driven cost pressure does not get absorbed quietly. It becomes a renegotiation trigger.

What the Data Is Telling Both Sides of the Table

Every renewal is a tariff conversation now. Contract renegotiation leads all tariff responses at 47% among acting buyers, the fastest lever available on already-committed spend. Vendors without a prepared pricing-flexibility narrative are walking into those conversations underprepared. Buyers who have not yet pulled this lever are leaving savings on the table.

The peer benchmark has moved. Thirty-five percent of technology leaders have moved beyond monitoring. Being in the 55% is either a deliberate posture or inertia, and the organizations that moved first are resetting the negotiation baseline everyone else will face next cycle.

Hardware demand strength in Q1/Q2 should be read with caution. Pre-buying is the most credible driver of the current hardware spending surge. Vendors should not anchor back-half forecasts to it; buyers who have not yet acted should not assume the pricing window stays open.

Concentration risk is being actively repriced. At 39%, supplier diversification is one of the top three tariff responses. Vendors with single-region supply chains are competing against alternatives that carry less risk in the buyer's model. Buyers with single-vendor exposure are paying a concentration premium that was not part of the original contract calculus.

Software and cloud substitution is the only structural hedge in the data. Twenty-eight percent of acting organizations are already moving in this direction. The gap between hardware pricing (5.5%) and software pricing (3.3%) is the mechanism. Vendors in tariff-insulated categories should be making this case explicitly; buyers should evaluate it on a timeline that extends past this quarter.

The Bottom Line

The tariff story is not a tariff crisis. It is a procurement rebalancing in a market that was already tightening. The behavior is concentrated in the third of the market that has chosen to move first, and that group is using the tools with the fastest path to leverage: contracts and hardware timing. The vendors and buyers paying closest attention to the gap between intent and execution will be best positioned when the next wave of adjustments lands.

The Spring 2026 Macro Views findings go deeper than tariffs. The full report covers spending intentions across cloud, software, hardware, and AI, with breakdowns by sector, company size, and region. Visit the Macro Views page to fill out the form to access the summary and complete report.